Anon

Communitypaywithanon.com

The NO-KYC crypto card 💳 The Anon Card lets you spend over 5+ #cryptocurrencies like cash online and worldwide 🌎 #bitcoin #Litecoin #USDT

Live preview

paywithanon.com

▶

https://paywithanon.com

Review

EditorialOverview

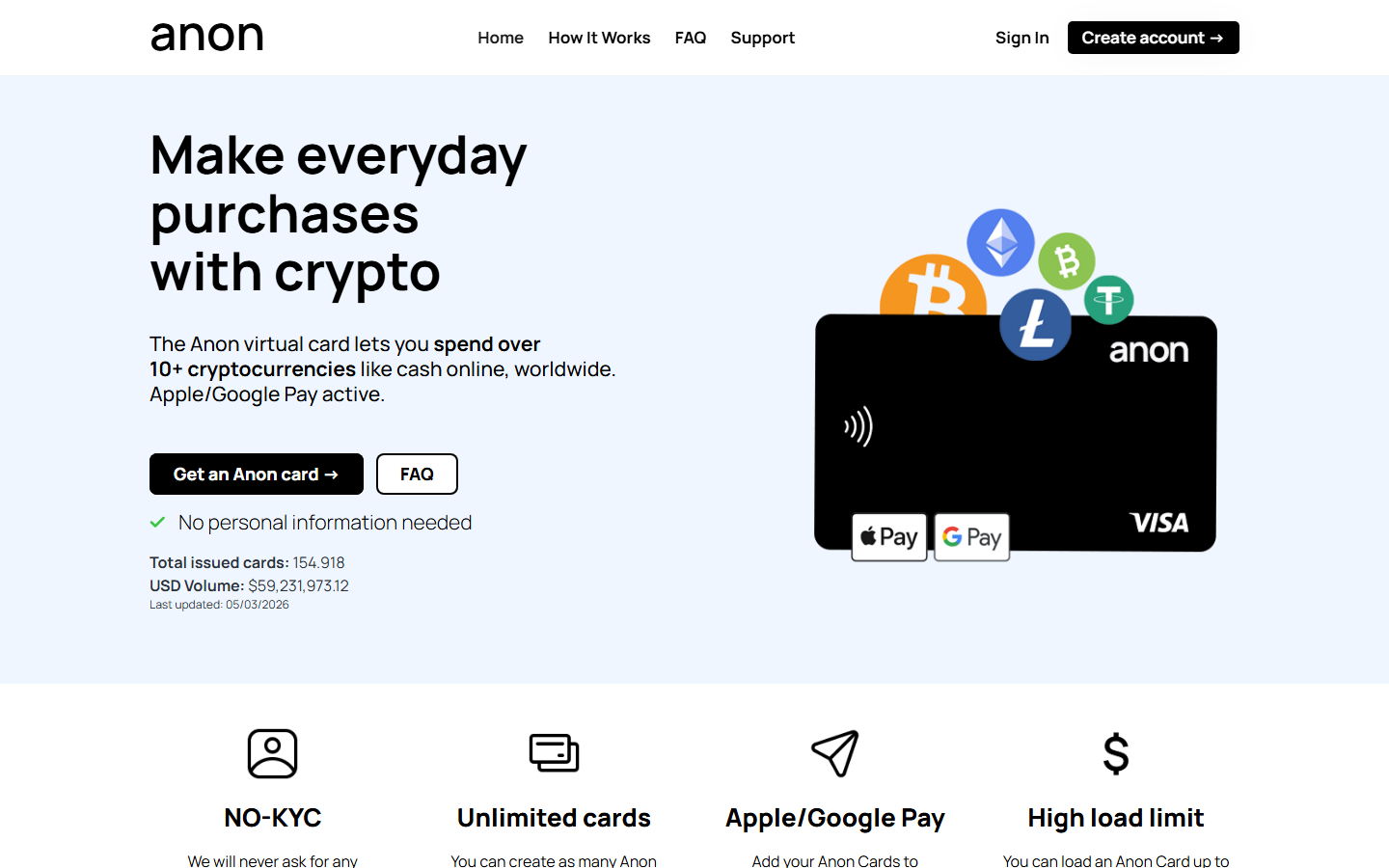

Anon is a no-KYC fintech platform offering virtual Visa debit cards that convert cryptocurrency to USD for online spending. Founded on a strict zero-verification policy, the service targets privacy-conscious users who want to transact without surrendering passport scans, proof of address, or biometric data. As of early 2026, Anon reports over 154,000 cards issued and nearly $60 million in cumulative USD volume, suggesting modest but real traction in the anonymous payments niche.

The model is straightforward: deposit crypto, get a dollar-denominated balance, generate virtual card numbers, and spend anywhere Visa is accepted online. Anon also supports peer-to-peer transfers between users and Apple/Google Pay integration for cards loaded with more than $500. The company is explicit that it is not a bank — cards are issued by partner financial institutions under Visa license, meaning traditional banking rails ultimately settle transactions.

Privacy & KYC

Anon sits at KYC Tier L1 — Anonymous in our framework. Account creation requires only an email address. No government ID, no selfies, no proof of residence, and no phone verification. The FAQ repeatedly emphasizes this as a permanent policy, not a temporary promotional threshold.

- IP logging: Not explicitly addressed in public documentation; assume standard server logs apply.

- Email requirement: Mandatory — the single identifying factor in the signup flow.

- Monero pipeline: XMR funding is a standout feature. Since Monero obfuscates on-chain traces and Anon skips identity checks, this creates one of the most anonymous spend-to-fiat corridors available in 2026.

However, anonymity ends at the card rail. Once crypto converts to USD inside Anon's system, transactions flow through Visa's monitored network. Merchants, card issuers, and Visa itself see standard payment metadata. Anon is anonymous at entry, not invisible at exit.

Supported assets & payments

Anon supports 10+ cryptocurrencies for balance funding. Verifiable assets include Monero (XMR), Bitcoin (BTC), Ethereum (ETH), Litecoin (LTC), Bitcoin Cash (BCH), and USDT. Crypto deposits auto-convert to USD upon arrival — users do not hold volatile coin balances within the app.

Card mechanics carry notable constraints. Virtual cards load up to $1,000 USD each, and users can create unlimited cards. Apple Pay and Google Pay activation requires a single top-up exceeding $500, gating mobile wallet convenience behind higher initial commitment. There is no physical card option; online-only spending limits utility for in-person commerce.

Crucially, funds cannot exit the ecosystem. USD balances are trapped — usable only for card loads, online purchases, or P2P sends to other Anon users. No crypto withdrawals, no cash outs, no bank transfers. This one-way design is a deliberate friction point that privacy seekers must weigh against the no-KYC benefit.

Security & custody

Anon operates on a custodial model. Your deposited crypto becomes Anon's crypto; you receive a USD claim, not segregated wallet access. The platform controls private keys, conversion timing, and balance availability. This is standard for card-issuing fintechs but represents a trust assumption that cypherpunks typically reject.

The trust score of 50/100 reflects this concentration risk. Anon Services, Inc. is a young fintech, not a chartered bank, with no public audit reports or proof-of-reserves documentation. Partner institutions issue the actual Visa cards, but user funds sit in Anon's layer. Regulatory pressure on anonymous payment channels is intensifying in 2026; a sudden freeze or operational shutdown would leave users with minimal recourse given the intentional lack of identity records.

Security features like 2FA, withdrawal whitelisting, or insurance are not detailed in crawled materials. Users should treat deposited amounts as spending money, not savings.

Who it's for — verdict

Anon fills a narrow but genuine niche: privacy-conscious individuals who need to spend crypto online without identity exposure. Journalists in sensitive regions, gig workers protecting financial metadata, or ordinary users fatigued by intrusive KYC questionnaires will find the email-only onboarding refreshing. The Monero integration is particularly valuable — few card providers accept XMR, let alone without verification.

That said, the 6/10 overall score and 65/100 privacy score signal meaningful tradeoffs. The custodial trap, Visa-network visibility, and absence of hard security disclosures drag down what the KYC policy gains. Users comfortable with moderate amounts, comfortable treating balances as disposable, and strictly needing online payment rails will extract the most value.

Skip Anon if you need physical cards, in-person anonymity, fund recovery options, or long-term storage. Embrace it if your priority is quick, pseudonymous online spending with Monero or Bitcoin — understanding that convenience and privacy exist in tension here, not harmony.

Community summary

Anon offers a pseudonymous virtual Visa card funded by 10+ cryptocurrencies including Monero, with zero identity verification required — though funds lock into a custodial USD balance with no withdrawal option.

Pros

- + True zero-KYC onboarding — only email required

- + Monero (XMR) funding accepted, rare among card providers

- + Instant card generation with no approval waiting period

- + Unlimited virtual cards up to $1,000 each

- + Apple/Google Pay support for higher-balance cards

Cons

- − Custodial USD balance with no crypto or cash withdrawals

- − No physical card — online spending only

- − Trust and transparency gaps; no audits or reserves disclosed

- − Visa network exposes transaction metadata despite anonymous funding

Attributes

3 signalsStrengths

No KYC mention

P+15

Accepts Monero

P+5

Cautions

Community contributed